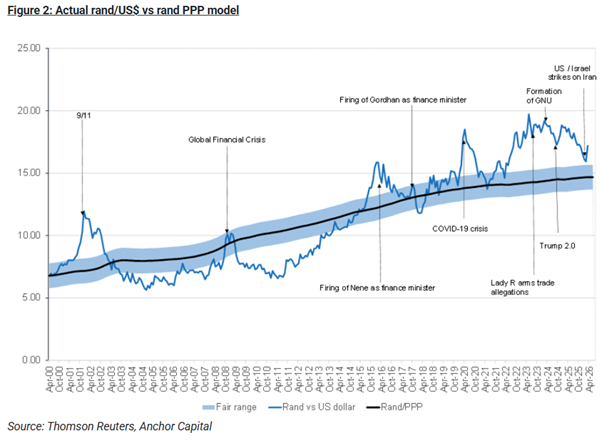

COLUMN - I really enjoy this chart on the rand from Anchor Capital.

It shows the rand against the US dollar over time, alongside what’s called a PPP model (the smooth black line).

In simple terms, the PPP line reflects where the rand should trade based on inflation differences between South Africa and the US.

The gap between the two is the risk premium investors attach to South Africa.

One thing that stands out is the steady upward slope of that PPP line. That’s not random. It reflects the fact that South Africa has historically had higher inflation than the US.

If inflation is 4% higher locally, you would expect the rand to weaken by roughly that amount each year over time.

At first glance, that sounds like bad news.

But there’s another side to it.

Higher inflation is typically accompanied by higher interest rates.

That’s where things get interesting.

While investors in the US might earn 3% on cash, in South Africa that number is often closer to 7% or 8%. So although the rand may weaken by 3% to 4% a year, you are being compensated through higher yields.

In simple terms, the currency move and the interest rate differential tend to offset each other over time.

It’s slightly counterintuitive, but it means that holding rands in a South African interest-bearing account has, over long periods, been more rewarding than holding dollars in the US, even after taking rand depreciation into account.

Looking at the chart, Anchor also overlays major events that have driven sharp moves in the rand. I see they have recently added the Iran escalation.

What’s interesting is that this move has very little to do with South Africa itself. It’s a global event, yet it still moves the rand.

That’s an important reminder.

We often assume the rand moves mainly because of domestic politics or economic conditions. In reality, it is highly sensitive to global capital flows and international risk sentiment.

If you go through the major moves on the chart, just over half are driven by global events, with the rest being local.

This is why we don’t make big currency bets in portfolios.

These forces are long-term, complex, and largely outside of our control.

We invest offshore not because we’re trying to predict currency moves, but because of the opportunities that exist globally that simply aren’t available in South Africa.

Matthew Matthee has a wealth management business that specialises in retirement planning and investments. He writes about financial markets, investments, and investor psychology. He holds a Masters Degree in Economics from Stellenbosch University and a Post Graduate Diploma in Financial Planning from UFS. [email protected]

‘We bring you the latest Garden Route, Hessequa, Karoo news’